Andy Bottrill, Regional VP at leading financial close solution ‘BlackLine’, discusses the collective role which people and technology have to play, in the ever-changing finance function of the future.

Finance and accounting is an industry of traditional standards; calculators, spreadsheets and manual input are all part of peoples’ daily routines.

However, whilst these tools have supported many people throughout their accounting careers, a lot of processes are no longer fit for the digital age, and businesses must innovate to remain competitive.

The biggest struggle for finance and accounting departments remains at month end – ensuring accounts close on time, with no mistakes. However, with the number of accounts to reconcile constantly increasing, the risk of human error is much higher.This is not affordable for businesses that want to remain a leader in their market.

Despite the challenges facing finance departments, such as increasing datasets, ensuring the quality and accuracy of reconciliations, as well as lack of time, many still fail to make the leap into the digital age and embrace automation over human, manual input.

Innovation is the only way forward, and whilst businesses can see the benefits, many are still reluctant to change. So what is holding finance departments back?

Mind over Matter

Many assume the financial cost of innovation is the main barrier to its adoption. In fact, more often than not, it is the traditional outlooks and mentalities of accounting professionals that represent the biggest challenges in modern finance departments.

It’s not only important to change the perception of technology among accountants, but also to reassure them that the risk of implementing new technology is outweighed by the benefits. Providing a better understanding of the benefits technology can bring will change the industry forever.

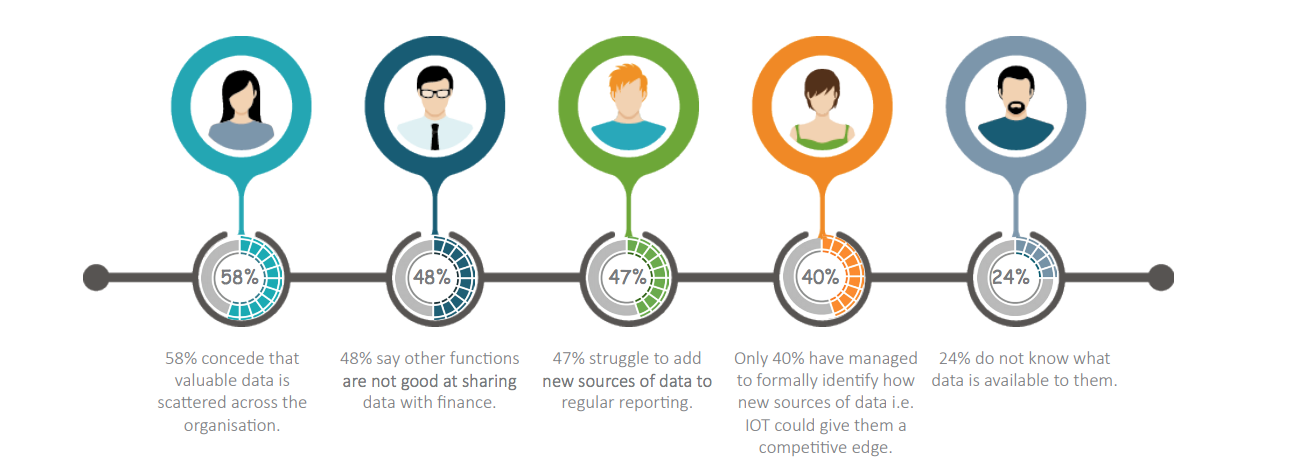

With 90% of the world’s data created in the last two years, the sheer volume of data being processed, especially in finance and accounting departments, is larger today than anyone could have envisioned.

But despite this exponential data increase, many accountants still use traditional tools such as paper, pen and calculator – or the ‘modern’ day equivalent, Excel – to manage the finances of multi-million pound companies.

Known as the ‘comfort blanket’ of the industry, spreadsheets are still the relied-on method of reconciliation for the month end and used by almost three quarters (71%) of accountants. [1] (The Future of the Finance Function, FSN, 2017). This Excel blanket may have worked in the past, but in the last 10 years we’ve seen a shift– especially in e-commerce – that has rendered manually produced spreadsheets inadequate as companies adopt a more digital approach.

This shift has resulted in the need to transition to solutions that can better handle large volumes of data. Though this transition seems daunting, the amount of time it will save and the number of errors it will remove should outstrip peoples’ fear of change. To achieve this, a shift in the culture of finance and accounting departments is needed, and this must be lead from the top down.

However, research found that only 6% of Chief Financial Officers (CFOs) [2] said they have a good grasp of the latest automation technology. With such a low figure at C-Suite level, it’s easy to understand how this lack of awareness can translate to other levels of the business, and ultimately throw up barriers to the adoption of new solution.

So how can finance leaders encourage innovation and trust in new technologies?

Culture Change through Education

To encourage change and innovation, I believe the best practice is to play an active role in changing the culture around you. To do so, you must present not only what workers are missing out on, but also how it can make everyday life easier for them.

In my experience, most accountants have cited their biggest challenges as month end reconciliation and the rising workload they are faced with, followed by poor accuracy and quality of work, as data is inputted manually. New technology available today can help to overcome all of these barriers. Offering real-time, transparent data enables finance departments to complete reconciliations on a daily basis. As a result, much of the workload is removed.

By automating processes that were previously done manually, error rates can be reduced and accuracy significantly improved.

Though new technologies, such as automation and AI, will enhance outcomes and roles across the board, the main challenge is bringing this realisation to the individuals who need to take the plunge and move from what they know. So what better way to encourage innovation, than by solving a clear problem? Remove arguably the most disliked task in accountancy – reconciliation – and transform it from a time-intensive manual task to one that is automatic and continuous.

Innovation Cost: Well worth it for Future Profits

Research has found that 43% of accountants already believe that invoicing will be obsolete by 2030, in addition to 80% of large organisations and a quarter of small organisations on track to adopt close automation by 2020 [3].

But now, I think what employees – especially accountants – need to see is hard data and facts.

You just have to look at the volume of data that passes through the finance department to understand the benefits and impact of innovation today – enabling timely, comprehensive tasks to be carried out in a matter of minutes with minimal margins of error. And the benefits to individual workers are also huge.

New technologies can overcome the challenges today’s accountants face; almost three quarters (70%) of finance and accounting professionals have said they have been able to spend more time helping other departments as a result of investing in new technologies.

[4] Lending a helping hand to other departments not only benefits the business, but also up-skills those in finance and accounting.

In the last year, streamlined automation technology (such as EiB Financial Analytics) reconciled millions of accounts, managed billions of transactions and saved departments significant costs in required adjustments.

Whilst we live in an increasingly digital business world, these physical, manual tasks are still a common part of the closing process. These traditional systems, however, are simply not enough to support the demands of businesses today – and though the cost of innovation may seem high, the rewards will be worth it.

Author: Andy Bottrill. Regional VP, BlackLine

Original Source: Global Banking and Finance Review

[1 & 2] The Future of the Finance Function, FSN, 2017

[3] Gartner

[4] IMA Report

Our Expert Opinion series seeks to provide insight, advice and information from thought leaders across the globe, in the fields of data, analytics, BI and MI. To contribute to our series, please contact lfarrugia@excelinbusiness.com